Written by: Krista E. Callahan-Caudill, M.A., Assistant Director of Learning Services, University of Kentucky, Kristen Jowers, M.S., & Nichole Huff, Ph.D., CFLE

Why Financial Literacy Matters for Emerging Adults

Financial literacy is a foundational life skill, much like learning to cook or preparing for a job interview. Emerging adulthood presents a critical window to create lifelong money habits, particularly for young adults. From understanding a first paycheck or leave and earnings statement (LES) to navigating credit, debt, and long-term goals, this stage is not just about understanding how money works, but laying the groundwork for informed financial decision-making.

Understanding Neurodivergence and Money Habits

While building financial skills can be daunting for anyone (at any age), neurodivergence can create unique considerations when learning and acquiring these financial literacy skills. According to the Cleveland Clinic (2022), neurodivergence is an umbrella term that refers to the ways in which some brains work differently for various reasons. In the US, 15-20% of young people live with some type of neurodivergence, ranging from autism spectrum condition to ADHD (NIH, 2022).

Every brain works a little differently, and teaching financial skills should build on individual strengths. Some conditions can affect how people process information, plan, or manage time. For example, many individuals with neurodivergent brains are skilled at recognizing patterns in data. This can be leveraged to help build better budgets and reflect on spending patterns. Other people thrive off routine, which can be a great foundation for setting up savings regimens and paying off bills.

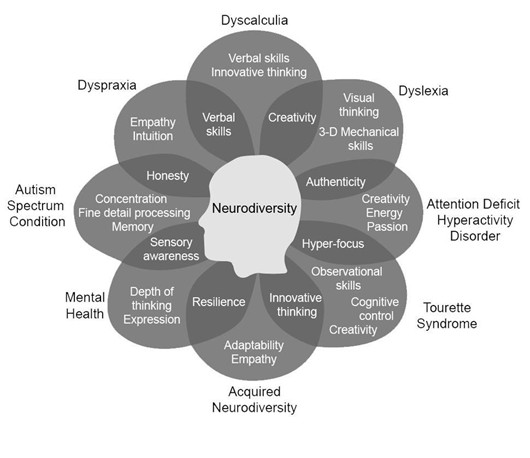

Consider this infographic from the National Institute of Health (2022) to identify several strengths of neurodiversity, including the specific ways these skills (e.g., honesty, hyper-focus, creativity, and innovative thinking) can be useful for managing finances.

Source: NIH (2022) Nancy Doyle: Overlapping Skills and Strengths of Neurodiversity

Tailoring Strengths to Financial Habits

Teaching new skills – whether financial or otherwise – should incorporate individual strengths. The best way to start is by taking small, manageable steps that help create sustainable habits. Below are six ways to leverage strengths for money management, including examples in italics:

1. Track spending: Set up simple routines, like tracking daily expenses.

- A young adult might use their ability to hyper-focus to track spending by setting up push notifications on a spending tracker app to stay on top of daily purchases.

2. Automate bills and savings: Automating tasks can reduce stress and ensure consistency.

- A young adult who thrives on a routine might set up automated bill payments to make sure bills are covered on time, even during the busy weeks of an upcoming permanent change of station.

3. Set savings goals: Use tools like spreadsheets, apps, or color-coded charts to make progress visible.

- A young adult who excels at visual thinking might set a clear savings goal (like $100 for a pair of shoes or gaming headphones) and track progress with a color-coded chart that clearly highlights milestones.

4. Monitor credit history: Track financial health by regularly reviewing credit reports. Free credit reports are available weekly: AnnualCreditReport.com

- A young adult who has observational skills might regularly review their credit report, quickly spotting any errors or inconsistencies.

5. Leverage technology, like apps and online financial education resources designed specifically for military families.

- A young adult with innovative thinking or adaptability might explore the SEN$E mobile app to use calculators and learning tools.

6. Celebrate progress with rewards, and keep financial goals attainable and concrete.

- A young adult may use their strengths in creativity, energy, or passion to come up with rewards for each time they reach a milestone.

Turning Differences Into Superpowers

When it comes to managing money, there’s no one-size-fits-all approach. This is what makes having unique brains an asset. Being neurodivergent often means having strengths that can help with tackling financial tasks in creative ways. Whether it’s using hyperfocus to dive deep into a budget plan, using attention to detail to track spending, or building on the love of routines to automate saving, differences can become some of the greatest financial superpowers. The key is to help individuals recognize those strengths and lean into what works with their brain, and not against it.

Want to learn more?

- Explore the OneOp series, Uniquely Wired: A Deep Dive into Diverse Cognitive Variations (https://oneop.org/series/uniquelywired/).

- Read the blog: Why Financial Skills Matter for Neurodivergent Children (https://oneop.org/2025/01/14/why-financial-skills-matter-for-neurodivergent-children/)

- The Academy | Military-Connected Youth Well-Being (https://oneop.org/series/2025academy/)

References

Cleveland Clinic. (2022). Neurodivergent. https://my.clevelandclinic.org/health/symptoms/23154-neurodivergent

National Institutes of Health. (2022, April 25). Neurodiversity. Division on Cancer Epidemiology & Genetics. https://dceg.cancer.gov/about/diversity-inclusion/inclusivity-minute/2022/neurodiversity

National Library of Medicine. (n.d.). Neurodiversity. https://www.nnlm.gov/reading-club/topic/331